Out with the Old, In with the New: The New York DSIPs and What They Mean for the Modernized Energy Grid

The traditional system we currently use for serving the needs of energy users is quickly going out of style. The energy grid is still relying on a system that was invented almost 100 years ago (hello, the 1930s called and they want their transmission and distribution lines back!). The old classic version of the grid has served an important purpose for getting energy to consumers reliably and safely, but today’s energy fashion is more demanding. While the old grid excelled at sending energy one-way from generators to consumers, the new energy grid needs to be able to accessorize by incorporating distributed energy resources (“DER”) such as solar and wind energy, active load management, and energy efficiency programs. DER will enable the development of a grid that is increasingly resilient, flexible, and adaptable to the needs of all energy consumers. In New York, a process is under way to try to bring these innovative new options online.

A modernized energy grid doesn’t happen overnight. States across the Northeastern U.S. are trying to figure out how to facilitate the transition from a traditional energy grid system to a more modernized grid. The Distributed System Implementation Plan (“DSIP”) process initiated by the New York Public Service Commission (“PSC” or “Commission”) may be one model for helping utilities make a smooth and efficient transition.

The Commission has required all electric service utilities to create and maintain comprehensive Plans detailing the processes by which they will transform the traditional one-way electric grid into a more dynamic and integrated grid that can manage two-way flows, is more resilient, and produces fewer carbon emissions. The DSIPs are a comprehensive source of information for the public and serve to consolidate several important pieces of New York’s Reforming the Energy Vision (“REV”) strategy. They are also intended to be a source of data and information to assist third-party DER providers with planning and investment. The new energy grid will require joint decision-making and planning between utilities, third-party providers, consumers, regulatory bodies, and other interested parties. This means that transparency and visibility are paramount to achieving a modernized grid.

The DSIP process is novel in that it has required utilities to make their internal decision-making more transparent and begin making joint planning decisions. This type of practice has potential for creating a collaborative environment that produces a constructive transition. The DSIP process has done well in New York to:

- Provide insight into key decision-making processes of utilities, especially regarding the use of DER in addressing system needs

- Provide a baseline for current data-gathering capabilities as well as capabilities regarding load forecasting and accommodating DER

- Create a space for joint decision-making and planning between utilities

- Involve stakeholders on various key issues

While the DSIPs that the utilities produced are important and useful, in many ways they fall short of what was expected of them. Some improvements that should be made to the DSIPs include:

- Valuable data – for example regarding hosting capacity, DER forecasting, and DER impacts on the grid – has not yet been included in the DSIPs and the utilities have not in many cases provided sufficient plans for providing the data

- Many of the plans that have been provided are a good start, but are still not sufficiently detailed or specific enough to be useful for the public and third-parties, for example, almost no timelines for implementation are provided

- There is a general lack of description regarding how various processes, such as forecasting and making decisions about using DER for system needs, will be re-assessed and evolved as technologies and data-gathering capabilities improve

- Stakeholder process has been utility-centric and lacked necessary oversight by the state energy regulatory body to ensure fair and meaningful engagement by all interested parties, including at the scoping stage of the process.

In sum, the DSIP process provides one model for states to facilitate the transition to the modernized energy grid, but they should look for opportunities to build on New York’s model. These first DSIPs were filed in 2016. Updated DSIPs will be filed in June 2018, giving utilities another opportunity to seek and receive the level of detailed data and planning that is needed to inform decision-making by other stakeholders and in other states.

Summaries of Important DSIP Focus Areas

Some of the most relevant aspects of the DSIPs are briefly described and assessed below. For more information about the New York DSIPs, read Acadia Center’s full Summary Analysis or the DSIP documents available in the proceedings.

Forecasting is the process by which utilities make predictions about energy load on the grid. Utilities also use forecasting to predict penetration of different DER technologies on the grid. These predictions have varied implications for what the grid needs to ensure reliable and safe power to all customers. The DSIPs provide a first glimpse into the calculations that utilities use and the impacts that DER are expected to have on forecasting. However, the DSIPs also reveal that utilities need to improve their forecasting processes and especially that they need to continue refining their methods for predicting DER penetration as well as DER impacts on the grid.

Utilities’ plans for accommodating and enabling DER on the energy grid are addressed in the DSIPs. As DER increase, their impacts on the grid increase. Distributed generation (such as wind and solar) for example, will increasingly be able to inject energy into the grid from various locations. The current energy grid can only manage a limited amount of distributed generation since it is currently only configured to manage energy flowing from a select few large generators into the homes and businesses of energy users. To optimize development of DER, third-party developers need to have detailed information about where DER can be accommodated and where DER might be most beneficial. The DSIPs provide important information about when and how this information will be available. They also describe their plans for streamlining the interconnection processes for distributed generators. These efforts will go a long way to reduce barriers for integrating DER with the grid, but the DSIPs also show a lack of preparation and planning for actively encouraging more DER. Increasing DER will be invaluable for enhancing resiliency and flexibility as well as decreasing carbon emissions.

Non-wires alternatives are DER that are procured by utilities to address the needs of the energy grid. Traditionally, utilities simply invest in more traditional infrastructure when the need arises. These types of upgrades are costly for the utility and thus for ratepayers. Alternatively, DER can be more cost-effective and can be used to avoid or postpone traditional infrastructure investments. The DSIPs provide clear analysis of the types of projects that they consider suitable for using non-wires alternatives. The utilities have defined a narrow range of projects that are suitable for these alternatives, and limiting the range of possible projects in this way means that there will be missed opportunities to address a wider range of system needs.

Advanced Metering Infrastructure (“AMI”) is important for advancing grid modernization efforts. It will enable utilities to vastly improve data-gathering capabilities and increase their ability to control energy load on the system. In the past, meters were only needed to measure energy used within a time frame, usually one month. With AMI, meters will be able to report hourly or even near to real-time data about energy use. This information will be invaluable for load forecasting and for better understanding DER impacts on the grid. Utilities will also be able to share data with customers – empowering them to better manage their own energy use. AMI also enables strategies to optimize the grid, like demand response, time-varying rates, and active load management. These strategies are based on increasing energy consumption during off-peak periods and decreasing it during peak hours. The DSIPs show that all utilities are planning to implement AMI over the next several years. However, the utilities are not consistent in how they present their plans for AMI roll-out. Some utilities provide excellent summaries or even include their full plans in the appendix of their DSIP. Other utilities provide almost no summary and simply refer to other proceedings.

Electric Vehicles will be key for achieving New York’s carbon emissions reduction goals. New York has made clear goals for increasing the number of electric vehicles on the road. This will require increased infrastructure, such as charging stations. Utilities are expected to be proactive about planning for and enabling the electric vehicle market. The DSIPs show that utilities are implementing pilot projects, mostly aimed at better understanding how these vehicles are used and charged, which will in turn help utilities better understand their impact on the grid. The utilities have also jointly produced a plan for creating an “EV Readiness Framework” which will guide their actions for preparing for electric vehicles. The DSIPs lack any concrete plans for going beyond pilot projects to implementing any wide-scale infrastructure investments for electric vehicles.

The DSIPs include investment plans that indicate how and where the utilities will spend money in the next several years to begin the transition to a modernized energy grid. Generally, utilities are investing in new systems and capabilities that will enhance data-gathering, load management, and DER integration, which will in turn increase grid reliability and efficiency. Utilities also need to invest in improving customer engagement by providing understandable billing and secure data exchange platforms.

EnergyVision 2030: What the numbers tell us about how to achieve a clean energy system

What impact will current efforts to expand clean energy markets in the Northeast have over time? Where can we do more to advance these markets? What specific increases in clean energy are needed to adequately reduce carbon pollution and meet targets for deep reductions in climate pollution? What does the data show about claims that more natural gas pipeline capacity is needed?

A few years ago, Acadia Center released a framework entitled EnergyVision, which shows that a clean energy future can be achieved in the Northeast by drawing on the benefits of using clean energy to heat our homes, transport us, and generate clean power. Many studies have shown that a clean energy future will improve public health, increase consumer choice, and spur economic growth by keeping consumer energy dollars in the region. States have started to move towards the future put forward in our EnergyVision framework supporting key clean energy technologies like rooftop solar, electric vehicles, and wind, and increasing investments in energy efficiency and upgrades to the grid.

But other voices have tried to slow or even block progress toward a clean energy future. Claims that the region needs more natural gas capacity continue to be made, most recently by the U.S. Chamber of Commerce, and states are not uniformly moving forward in all areas of clean energy development. Efforts to reform the power grid vary from state to state, and the data needed to identify what our energy system could look like in a few years and what contribution clean energy can make has not been gathered.

To fill these important information gaps and help answer these questions, Acadia Center undertook a comprehensive analysis of the Northeast’s energy system. Using a data based approach, we looked at where current state and regional efforts to expand clean energy stand and what emissions reductions and growth in markets for clean energy technologies those efforts will produce. We then examined what expansions in clean energy are needed to attain state goals to reduce climate pollution. The result is EnergyVision 2030, an analysis of the energy system that provides a clear pathway towards a clean energy future that empowers consumers in the Northeast.

EnergyVision 2030 demonstrates that the Northeast region can be on track to a clean energy system using technologies that are available now. In the last several years, clean technologies have advanced rapidly, and they offer states an unprecedented opportunity to transform the way energy is produced and used. For example:

- The nation’s first offshore wind project has recently come online in Rhode Island

- Electric heat pumps that work in the cold climates of the Northeast are now readily available

- There has been a dramatic increase in the number of electric vehicle options on the market

- Efforts to modernize our electric grid are underway in several states

- Onshore wind is now the lowest-cost electric resource in some reports

- Massachusetts and Rhode Island have redefined the levels of energy efficiency that can be consistently achieved.

And the list goes on.

To determine what growth in key clean energy technologies is needed, Acadia Center used a well-respected model1 to analyze the energy system as it might look in the year 2030 under different conditions. First, EnergyVision 2030 shows what the energy system would look like under current trends, and then if policies were put in place to expand markets for newer technologies more quickly—at rates leading states are already achieving.

With this approach, EnergyVision 2030 finds that the first generation of climate and energy policies has successfully built a foundation for progress. Energy efficiency, renewable portfolio standards, and the Regional Greenhouse Gas Initiative (RGGI) have all contributed to declining emissions since the early 2000s.

To be on track to meet state targets for emissions reductions the region needs to achieve a 45% emissions reduction by 2030.2 We used this 45% reduction as a target to develop our “Primary Scenario,” which features individual targets for clean energy technologies that together would reduce emissions 45%. We also modeled what it would take to get to a 50% reduction, in our “Accelerated Scenario.”

Policy changes drive both of these scenarios, which would see lagging states catch up to leaders like Massachusetts in energy efficiency and other areas, expand and extend renewable portfolio standards as New York has recently done, and grow markets for newer clean energy technologies like electric vehicles and cold climate heat pumps. In other words, if all states did what leading states are doing in each area—if they expanded building heat pumps like Maine, electric vehicles and solar like Vermont, energy efficiency like Massachusetts and Rhode Island, and utility reform like New York—the Northeast would achieve its emissions goals.

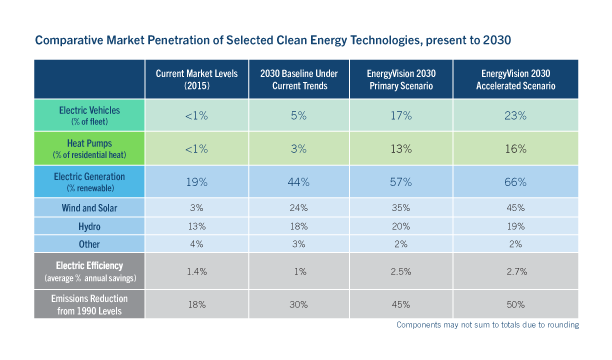

The table below shows how much selected clean energy technologies will expand by 2030 under current trends and in the Primary and Accelerated Scenarios.

To foster these clean energy markets, states can redouble their efforts and create a second generation of clean energy policies building on their initial success. The following policy recommendations will help make this possible. A more complete list is available at 2030.acadiacenter.org.

Clean Energy:

- Extend and increase rooftop and community solar

- Expand Renewable Portfolio Standards

Electric Vehicles:

- Strengthen market for electric vehicles through consumer incentives and better electric rate design

Lower-Cost Heating:

- Increase the market for heat pumps through incentives and education

- End policies that promote natural gas pipeline expansion

Electric Grid:

- Modernize and optimize the energy grid

- Reform utility incentives and regulation to better align them with state policy goals

EnergyVision 2030 combines detailed data analysis and policy recommendations to provide a tool for policymakers, advocates, and other stakeholders to demonstrate both why state-level policy changes are needed and what we can do to make those changes happen, putting us on the path to a clean energy system. As with the first generation of clean energy policies, results can take significant time to accumulate, so action is needed now to ensure the region is ready to meet 2030 goals. EnergyVision 2030 gives us the targets and tools we need to begin working toward those policy changes today.

EnergyVision 2030 is available as an interactive website and in printable formats at 2030.acadiacenter.org.

1 Long-range Energy Alternatives Planning (LEAP) system from Stockholm Environment Institute

2 45% emissions reduction from 1990 levels

EnergyVision 2030 FAQ

Frequently Asked Questions about EnergyVision 2030

What is EnergyVision 2030?

EnergyVision 2030 is a data-based analysis of options to expand clean energy resources in New York and the six New England states. It examines where current efforts can lead, how consumer adoption and market penetration rates can grow, and what increases in clean energy efforts are needed to attain emissions goals.

EnergyVision 2030 shows that advances in technologies that are now readily available, from heat pumps to electric cars to solar panels, create the means for states to advance a consumer-friendly energy system by increasing adoption in four key areas—grid modernization, electric generation, buildings, and transportation.

Why did Acadia Center prepare it?

Acadia Center prepared EnergyVision 2030 to provide a pathway for policymakers and others in the Northeast to show how market-ready clean energy technologies can modernize the energy systems, give consumers better options to control energy costs, and advance economic growth, while dramatically reducing climate pollution.

What are the key takeaways from the study?

States can achieve a modern clean energy system using available technologies, achieving a 45% emissions reduction by 2030, if policies are enacted now to foster and expand adoption of clean energy resources.

How does EnergyVision 2030 present the data?

EnergyVision 2030 uses the results from Acadia Center’s modeling to describe how much states should increase each clean energy technologies to shift the energy system. EnergyVision 2030 then offers detailed policy recommendations with policy options that states can use to achieve these results.

How can the information be used?

Information presented in EnergyVision 2030 shows the incremental gains needed in key clean energy areas for the region to achieve reductions in climate pollution and build robust clean energy economies. Advocates, stakeholders, and policymakers can use the information presented in EnergyVision 2030 to focus on where to expand current policies that will have the most impact or oppose policies that will move the region off this path. In many cases, states already have the policy tools they need to increase adoption of these technologies; they must simply improve and accelerate existing mechanisms to achieve the goals set in EnergyVision 2030.

What was the methodology?

EnergyVision 2030 uses the Long-range Energy Alternatives Planning System (LEAP) model from Stockholm Environment Institute to project a detailed forecast of energy consumption in all sectors and an emissions trajectory. Acadia Center incorporated the U.S. Energy Information Administration (EIA) Annual Energy Outlook (AEO) forecast, the ISO New England and New York ISO electric ’s Capacity, Energy, Loads, and Transmission (CELT) forecasts, and other data sources as appropriate. The LEAP model contains an electric dispatch model to simulate the electric system, determine the generation mix and ensure that there are sufficient resources to satisfy peak demand for power in summer and winter.

Why a 45% emissions reduction?

The scientific consensus is that to avoid the worst impacts of global warming, the U.S. needs to reduce emissions by 80% from 1990 levels by 2050. States must reduce emissions 45% by 2030 to be on a trajectory to meet that goal, i.e. if a straight line were drawn from the present emission levels to the required 2050 levels, the region would hit a 45% reduction in 2030.

Why 2030?

Most states in the region have committed to reduce emissions 80% by the year 2050 in some form, and several have goals for emissions reductions in the interim period. Building markets takes time and has cumulative impacts, so acting now is critical. 2030 is closer than it seems but offers states sufficient time to reach the clean energy levels outlined in EnergyVision 2030 if they take action in the next two to three years.

What does EnergyVision 2030 tell us about the economy?

In developing EnergyVision 2030, Acadia Center did not model how increases in clean energy technologies and processes will impact local economies. Numerous studies, including some by Acadia Center, show the economic benefits of shifting from paying for imported fossil fuels to investing in local clean energy improvements like those presented in EnergyVision 2030. These benefits include stronger local economies, local job growth, and significant consumer savings.

Does EnergyVision 2030 address calls for more natural gas as a “bridge fuel”?

EnergyVision 2030 analysis shows that the current and planned pipeline capacity in New England will be sufficient to meet the region’s needs as expanding clean generation and energy efficiency reduce demand. Adding new pipeline capacity to the region would cost ratepayers billions of dollars and would lock the region into higher-emission gas generation for decades.

RGGI Emissions Fell Again in 2016

Declining Emissions Signal Need for Reform

In advance of expected actions by the Trump administration to remove or weaken federal climate protections, the Northeast’s pioneering climate program continues to see reductions in carbon pollution, reflected by today’s three-year low auction clearing price. Member states must now strengthen the Regional Greenhouse Gas Initiative to preserve the program’s effectiveness and signal commitment to continuing bi-partisan climate leadership.

Introduction

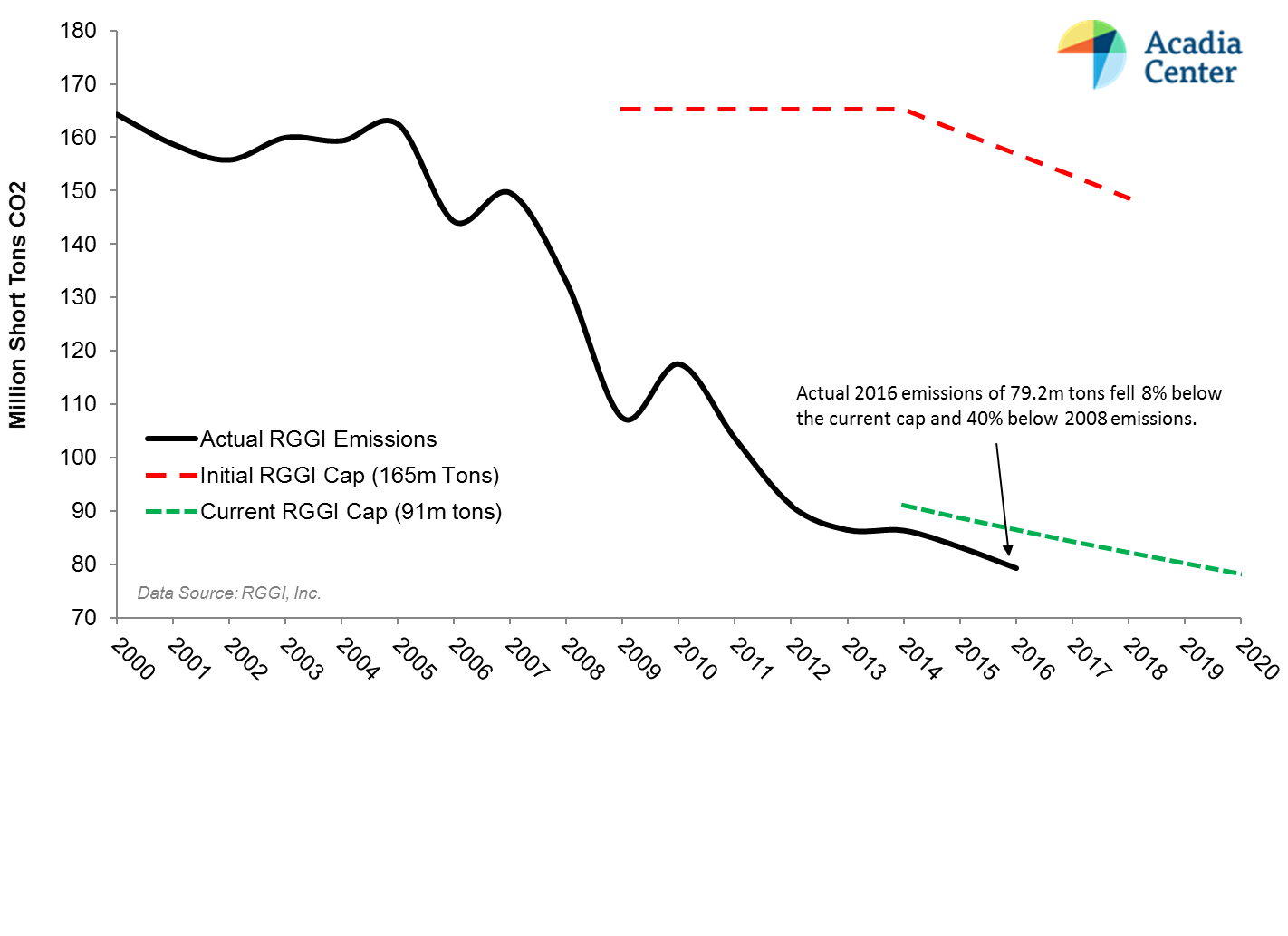

CO2 emissions from power plants have been steadily declining across the nine states of the Regional Greenhouse Gas Initiative (RGGI) for the last decade, and in 2016 fell 8.4 percent below the emissions cap. Since the program began in 2009, the decarbonization of the electric sector has been a major victory for the environment, health and economy of the region. Continued investments in clean energy and complementary climate policies in the participating states will help to achieve greater emissions reductions, but the RGGI states must do more to build on their first-in-the-nation program. Through the current Program Review,1 the participating states should strengthen RGGI to align the program with the current emissions trends and future climate goals.

Emissions

RGGI CO2 emissions fell to 79.2 million tons in 2016, a 4.7 percent decrease from 2015, marking the sixth consecutive year of power-sector emissions declines. Since 2008, the year before RGGI began, emissions are down 40.4 percent.

While several factors including growth in renewable energy, efficiency improvements, and fuel-switching have contributed to regional emissions reductions, a large share of these reductions has been attributed to the RGGI program.2 By establishing a price on carbon emissions and generating revenue for clean energy investments, RGGI has accelerated the transition to a cleaner electric sector. Increases in energy efficiency and growth in renewable energy output will enable the RGGI states to continue to achieve ambitious emissions reductions.

Figure 1: RGGI Emissions Continue to Fall

Market Dynamics

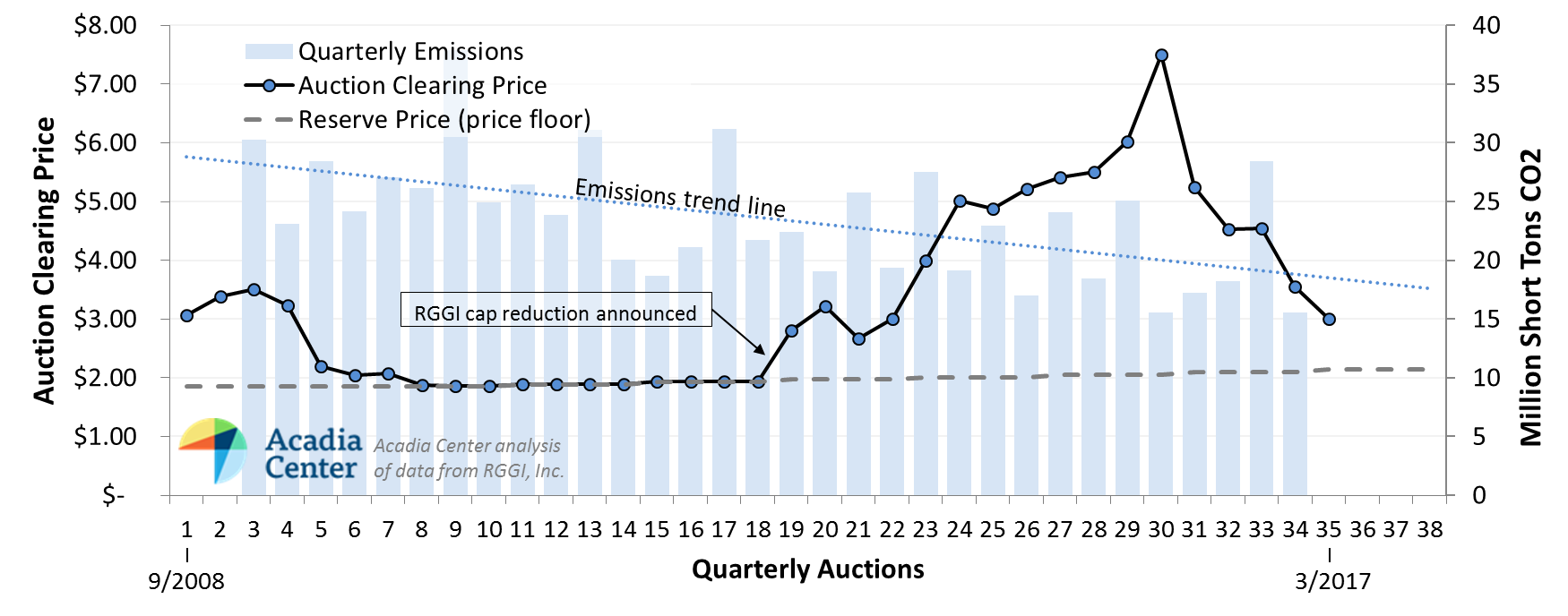

Auction Results

RGGI’s success has resulted in lower-than-expected emissions, which, in turn, have resulted in lower-than-projected compliance costs. With annual emissions falling below the RGGI cap in each of the program’s first eight years, there is an excess of allowances in circulation, leading to low allowance prices. Following ten consecutive auctions in which the auction clearing price was determined by the price floor—the lowest price at which allowances will be sold at a given auction—the RGGI states decided to reduce the cap by 45 percent. That decision had immediate impacts on the RGGI market, driving increased demand for allowances. Increased RGGI allowance prices proved to be temporary, however, as continued emissions reductions have outpaced the decline of the recently adjusted cap, creating an allowance oversupply. These conditions have resulted in falling allowance prices, with Auction 35 clearing at a three-year low of $3.00, 15 percent below the previous auction and 43 percent below the clearing price from one year ago.

Figure 2: Allowance Oversupply Leads to Low Auction Prices

Allowance Oversupply

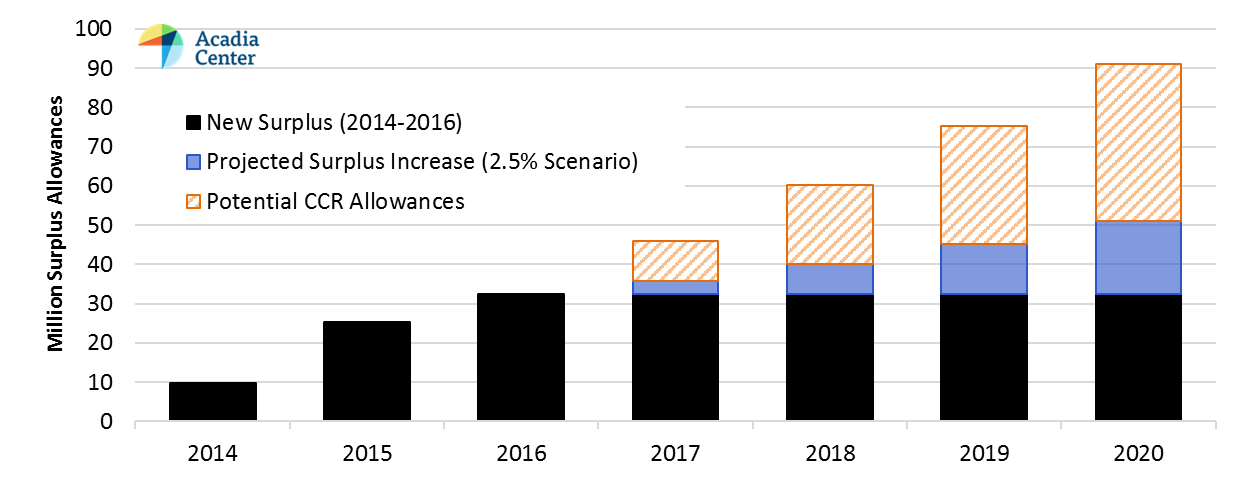

RGGI, like nearly all emissions trading programs, has struggled with an oversupplied market. Emissions reductions have been achieved more quickly and cost effectively than projected, creating a large gulf between cap levels and actual emissions, as shown in Figure 1. This has led to a market flooded with low-priced allowances, diminishing the program’s impact and undermining the environmental integrity of the cap. Recognizing these problems, the RGGI states agreed during the previous Program Review to gradually eliminate allowances banked prior to 2014 by adjusting 2014-2020 cap levels downward.3

This innovative strategy has proved effective, but a new surplus of allowances has been accumulated since 2014, and we expect it to increase through 2020 as trends that have contributed to the decline in emissions (growth in renewable energy, efficiency improvements, and fuel-switching) continue to bring emissions down.

In the first three years under the new cap, emissions have fallen below cap levels by 4.7 million tons (2014), 5.6 million tons (2015) and 7.3 million tons (2016). Over these three years all available allowances have been purchased, creating a surplus of 17.6 million tons. Additional allowances purchased from the Cost Containment Reserve (CCR) have added to the surplus, introducing 15 million additional allowances without corresponding emissions to balance the market. This brings the new surplus to 32.6 million tons, as shown in Figure 3. If emissions follow projections under recent ICF modeling of a post-2020 2.5% cap decline,4 the surplus will grow to 52.8 million tons through 2020. If CCR allowances are purchased, that figure could grow by up to 40 million tons.

Figure 3: Allowance Surplus, 2014-2020

Need for Market Reform

The emissions reductions achieved by the RGGI states have been a tremendous success, but program reforms will be necessary to ensure that this success continues. As detailed in Part II of our RGGI Status Report: Achieving Climate Commitments,5 the RGGI states should make the following changes to strengthen the program:

- Establish a 2021-2030 cap that declines annually by 5% of the 2020 baseline;

- Commit to an adjustment for banked allowances accumulated from 2014-2020;

- Eliminate the CCR or increase CCR price triggers to ensure that CCR allowances are only purchased during periods of exceptionally high demand;

- Establish an Emissions Containment Reserve6 to capitalize on emissions reductions and to protect against future allowance oversupply; and

- Increase the auction reserve price to at least $4/ton to maintain a meaningful price on carbon emissions.

1For more information on the current RGGI Program Review, see: http://rggi.org/design/2016-program-review

2Why Have Greenhouse Emissions in RGGI States Declined? An Econometric Attribution to Economic, Energy Market, and Policy Factors, Brian Murray and Peter Maniloff, Duke Nicholas Institute, August 2015. Available at: https://nicholasinstitute.duke.edu/environment/publications/why-have-greenhouse-emissions-rggi-states-declined-econometric-attribution-economic

3This adjustment was conducted in two steps; one adjustment to account for allowances banked during the first control period (2009-2011) and a second adjustment for the second control period (2012-2014). For more information, see: https://www.rggi.org/docs/SCPIABA.pdf

4IPM modeling conducted by ICF for RGGI, Inc. available here: http://rggi.org/design/2016-program-review/rggi-meetings

5RGGI Status Report Part II: Achieving Climate Commitments, Acadia Center, August 2016. Available at: http://acadiacenter.org/wp-content/uploads/2016/08/Acadia-Center_RGGI-Report-2016_Part-II.pdf

6The Emissions Containment Reserve (ECR) was first proposed by the RGGI states during the November 21st, 2016 Stakeholder Webinar: http://rggi.org/docs/ProgramReview/2016/11-21-16/2016_Nov_21_ECR_Presentation.pdf. For more information on how the ECR might function, see: http://www.rff.org/events/event/2017-02/emissions-containment-reserve-rggi-how-might-it-work

An Ode to Docket 4600

As told through a series of haiku:

I drove to Warwick

In a blue electric car

The chargers were full

Those in the know, know

Rhode Island utilities

Governed in Warwick

Fifty-four miles left

Should be plenty to get home

I am risk averse

Endure long meeting

With many energy geeks

Time-based rates for cars

Leafs swap spots at lunch

Brain can’t take much more rate talk

Level 2 charging

Start up in silence

I pause a moment, and breathe

Rate case up ahead

Can New England Steal California’s Storage Thunder?

Clean energy rivals New England and California are racing toward a new prize: leadership on energy storage. Both coasts have been leaders on energy efficiency, renewables deployment, and electric vehicles (EVs), and storage is the logical next step to improve system efficiency and back up intermittent wind and solar as they are increasingly adopted.

The benefits of storage are clear and increasingly well-recognized. Storage deployed at scale will serve the same purpose as warehouses and refrigerators in our food system by rationalizing an energy grid that is massively overbuilt to match supply and demand every second of every day. This logic is backed up by analysis from the Massachusetts’ Department of Energy Resources (DOER) showing that the top 10% of peak demand hours drive 40% of energy costs, and storing energy to meet these peaks would provide $3 billion in energy system benefits each year. According to a recent study from UC Berkeley, storage can also produce significant public health benefits by avoiding reliance on dirty ‘peaking’ power plants that are often located in marginalized urban areas.

Massachusetts Leadership

In the race for energy storage in the Northeast, Massachusetts is taking an early lead. Under energy diversity legislation passed this summer, DOER can act to meet the storage target it recommended—600MW by 2025—which proportionately would be far larger than California’s mandate. The legislation also cleared an important practical hurdle by authorizing utilities to own storage, and, so long as third-party owners are protected to ensure competition, political support for energy storage should remain strong.

An overall mandate would build on efforts already underway in the Commonwealth. DOER is offering $10 million for demonstration projects through the Energy Storage Initiative. The Massachusetts Clean Energy Center has invested $9 million in storage-related initiatives and is serving as a match-maker for storage developers and potential customers. Under the new solar incentive mechanism being developed, bonus incentives for storage are being considered in the range of two to seven ¢/kWh, based on storage duration (kWh) and power (kW) relative to solar capacity. Within energy efficiency plans that invest $700 million per year, utilities are piloting demand management programs integrating thermal and battery storage, and attention to demand resources is likely to increase as peak demand flatlines, overall consumption declines, and the focus on improving system efficiency at all levels grows.

New Tool in the Energy Toolbox

Across the Northeast energy storage is gaining favor as an alternative to more expensive and often difficult-to-site transmission and distribution (T&D) system upgrades. In Boothbay Harbor, Maine, cheap energy available at night is stored in ice that is then used to cool buildings on hot summer afternoons. In conjunction with targeted efficiency, solar, and demand response, storage is being deployed instead of an $18 million transmission upgrade. At a larger scale, in New York ConEd is investing $200 million in storage, targeted energy efficiency, distributed generation and demand-response in lieu of a $1.2 billion substation upgrade. The potential for eye-popping T&D savings (in addition to other energy system benefits) contributed to a proposed rule from the Federal Energy Regulatory Commission that would require all Regional Transmission Operators to remove barriers impeding storage from providing energy, capacity, and ancillary services. This clear directive will help drive the grid operator ISO-NE to take necessary steps to enable storage, including compensating storage for rapid response capabilities, opening markets to smaller storage facilities, and allowing storage to provide multiple services simultaneously. Large scale energy storage could additionally help replace retiring nuclear and coal capacity in Southeast Massachusetts/Rhode Island (potentially pairing directly with offshore wind in a coal-to-clean energy conversion at the soon-closing Brayton Point plant) and address expected load growth in the greater Boston area.

Complementing top-down reform, several states are pursuing grid modernization processes in order to capitalize on declining costs and technology advances for energy storage and other distributed energy resources. New York’s Reforming the Energy Vision has received the most attention, but REV does not stand alone. Massachusetts utilities filed Grid Modernization plans including energy storage projects and pilots in August of 2015, and while the plans need improvement to ensure unified progress toward truly modern grids, the process has begun. Meanwhile, Rhode Island is pursuing a truly bottom-up approach by using distributed resources to meet energy system needs, and grid modernization proceedings were recently initiated in New Hampshire.

Resiliency and Preparedness

Because of its resiliency and preparedness, storage is increasingly recognized for its security advantages. The vulnerability of the grid to cyber-attacks was made clear in Ukraine, and physical attacks on critical grid infrastructure have recently increased. Weather-related outages will also increase with climate change-fueled extreme weather. As we grow ever more dependent on electrical devices, the importance of grid security expands accordingly.

Storage alone can provide backup power, and pairing storage distributed generation offers steady supply when the grid is down. In recognition of these benefits, Massachusetts put $40 million into the Community Energy Resiliency Program to support solar plus storage projects at schools that double as emergency shelters, hospitals, and other critical facilities. Following storms that caused major power outages, Connecticut established a microgrid grant and loan program that is currently deploying $30 million in funding.

And the Winner Is…

California receives the most attention for energy storage, and with real progress toward a bold procurement mandate the attention is deserved. However, unique conditions in the Northeast—aggressive renewable energy targets, relatively high energy prices, and difficulty siting traditional infrastructure—make the region ripe for storage.

At this stage the race for energy storage leadership is just getting started, and the ultimate winners will be customers and the climate, as storage deployment ramps up, costs decline, and our entire energy system becomes more efficient and cleaner.

This blog post also appeared as a guest post on UtilityDive.com. See it here.

New York Proposes New Rates for Distributed Energy

This blog was co-authored with Miles Farmer, Clean Energy Attorney at Natural Resources Defense Council.

The New York Department of Public Service has proposed to change the way distributed energy resources (like community solar and small wind projects) are rewarded for the benefits that they provide to the electricity system. The Department released a landmark report in its “Value of Distributed Energy Resources” proceeding, recommending a methodology by which these resources can receive credits that align more closely with their true value to the electricity system. Acadia Center and NRDC have been involved in the collaborative process around the report’s creation, and here we examine what these proposed reforms hope to accomplish, give initial feedback, and look toward next steps.

This report marks the latest step in the state’s ambitious Reforming the Energy Vision (“REV”) initiative. REV aims to create a more consumer-centric, efficient, resilient, and cleaner energy system. The Department’s report focuses on reforming an electricity rate structure known as “net energy metering,” where credit for clean energy generation is set equal to the retail rate. Reforms to net energy metering have been a controversial topic across the country for the last several years. Some states have proposed successful new approaches. California, for example, is phasing in time-of-use rates for most customers that recognize when electricity generation is most valuable.

From the outset, New York’s Value of Distributed Energy Resources proceeding has sought to better align credits for community solar and other distributed generation resources with their value to the system. New York’s current net energy metering policies are simple, easy for customers to understand, and have proved to be effective incentives for investments in clean energy, so revising methods for net metering presents risks. A new ‘value-based’ crediting system is more complex by its very nature. But if done correctly, aligning credits more closely with benefits created by distributed generation has the potential to incent more efficient investments in the electric system. Acadia Center discusses value-based crediting here.

The staff report is a good start to a long-term iterative process. Throughout this process, Acadia Center and NRDC will be closely analyzing the report and offering recommendations for improvement. On first review, Acadia Center and NRDC find that the report recommends many approaches to important issues that are worthy of support:

- It protects existing projects from unexpected changes and allows mass market development of small rooftop projects to continue under traditional net energy metering, providing continuity.

- It provides credit to projects for their environmental value, with a floor at the social cost of carbon, pursuant to the New York Public Service Commission’s previous Benefit-Cost Framework Order.

- It provides for a ‘market transition credit’ that incorporates some values that cannot be accurately calculated at this time, recognizing limits in current techniques to estimate the value of benefits provided by distributed energy resources.

- It adopts monetary crediting, where each kilowatt hour generated is translated into a monetary amount based on the value it provides. This approach is more flexible and allows for smarter pricing than traditional volumetric crediting (which tracks only the amount of electricity generated and cannot accommodate details like the time at which the electricity was generated).

When creating a “value-based” crediting system like the Department’s proposal, the most difficult task is to develop a method for calculating the value of each of the benefits that distributed energy resources can provide. These benefits include energy, capacity (the availability of the system to provide electricity at times of peak demand), transmission and distribution value (because distributed energy resources like rooftop solar reduce the need for infrastructure to send electricity to customers), environmental and public health value, and other values that are more difficult to quantify. In practice, there are many ways to define and calculate the value of each of these components. However, the precise methods chosen have significant consequences for what investments will be made and how resources will be operated. Certain methods offer different tradeoffs. For example, using dynamic credit values may allow a resource to respond in real time to system needs, but they set less predictable values that might prevent investors from putting capital into beneficial resources.

The staff report effectively balances these goals in a manner that should facilitate continued growth of the solar industry in New York. It provides a good framework for further refinement, and we look forward to working with the Department and other parties to evaluate it further and carry out additional improvements.

The report also reflects the inclusive approach taken by the New York Department of Public Service. The Department facilitated a collaborative process to allow utilities, solar developers, customer representatives, environmental groups, and others to work together and provide input on a variety of issues including how the values of these different components should be calculated. Department staff has listened carefully to the concerns of all parties, including a range of detailed suggestions by Acadia Center and NRDC.

New York’s approach to valuing distributed energy resources is new and innovative, and regulators in states across the country will be examining it closely. We look forward to continuing to work collaboratively on these important issues as New York refines its proposal and builds upon it in future years.

Finding New Frontiers: Clean Energy on Aquidneck Island

This summer, an Acadia Center blog post highlighted the clean energy moment happening in Connecticut. Policymakers in that state are currently deciding what its energy future will look like for years to come, and stakeholders must take notice—but Connecticut isn’t the only state having a clean energy moment. In fact, you might say the whole region, country, even world is having a clean energy moment. At Acadia Center, we strive to capture a vision that will help more communities, of whatever size, embrace these moments, and recently in Rhode Island we found ourselves in a room with more than one hundred locals excited by that vision.

At Acadia Center’s latest forum, community members came together from Aquidneck Island’s three towns to celebrate achievements, explore possibilities, and identify specific  opportunities for using clean energy locally. The audience heard from two state representatives, Lauren Carson and Deborah Ruggiero, and two state commissioners, Marion Gold of the Public Utilities Commission and Carol Grant of the Office of Energy Resources. Attendees had the opportunity to engage with these four women as well as with panelists from National Grid, People’s Power & Light, the City of West Warwick, and the Rhode Island Infrastructure Bank. Acadia Center’s Rhode Island Director, Abigail Anthony, also presented the basic principles of EnergyVision, with particular emphasis on Community|EnergyVision.

opportunities for using clean energy locally. The audience heard from two state representatives, Lauren Carson and Deborah Ruggiero, and two state commissioners, Marion Gold of the Public Utilities Commission and Carol Grant of the Office of Energy Resources. Attendees had the opportunity to engage with these four women as well as with panelists from National Grid, People’s Power & Light, the City of West Warwick, and the Rhode Island Infrastructure Bank. Acadia Center’s Rhode Island Director, Abigail Anthony, also presented the basic principles of EnergyVision, with particular emphasis on Community|EnergyVision.

The event was called “Solar and Beyond” and it highlighted the community’s solar potential by featuring sponsors from solar companies, who were available to answer questions before and after the panels (a big thank you to Newport Solar, RGS, and Direct Energy Solar). Other topics that drew interest included Block Island’s new offshore wind farm, transportation’s role in the clean energy future, energy efficiency, and the possibility of going 100% renewable.

Acadia Center was privileged to have two excellent partners in this venture, the Aquidneck Island Planning Commission (AIPC) and Emerald Cities Collaborative. We are excited to continue working with these organizations to harness the momentum built at the forum and support effective policies to make the community’s vision a reality. Working with AIPC and Emerald Cities, Acadia Center is developing a forward-looking policy agenda to remove barriers to community energy and build a coalition of support from municipal leaders on Aquidneck Island. Acadia Center is promoting several key actions that Aquidneck Island leaders can take to advance community energy, including:

- Expand the use of local energy resources to avoid the construction of infrastructure projects and reduce costs. In December, the state’s Energy Efficiency & Resource Management Council will propose reforms to utility planning that are designed to proactively deploy energy efficiency and distributed energy resources, like solar, in “highly-utilized” areas of the electric grid to ensure energy reliability for all.

- Adopt Property Assessed Clean Energy (PACE) programs to provide long-term clean energy financing for businesses and residents. Aquidneck Island towns should authorize Commercial PACE, which offers financing for clean energy projects on commercial, industrial, agricultural, non-profit, and multifamily properties. Municipal leaders should also advocate for strong consumer protection elements in the roll-out of Residential PACE in Rhode Island.

- Expand access to community solar. Rhode Island laws passed in 2016 create more opportunities for residential and qualified low- and moderate-income housing developments to benefit from solar projects. However, the Community Remote Net Metering program is currently capped at 30 MW. Aquidneck Island leaders can support advocacy efforts to remove this cap and promote community solar projects.

Over the coming months, Acadia Center will work with AIPC and Emerald Cities to build a strong coalition of support for these policies and others. Together we hope to lay a foundation for community energy in Rhode Island that will reduce greenhouse gas emissions and better serve consumers. By seizing this clean energy moment, Aquidneck Island will secure an energy future that is reliable, cost effective, and community driven.

In a rapidly changing world, what do we mean by RGGI leadership?

Never before has the urgency of climate action been so apparent, demonstrated by record high temperatures and unprecedented drought. Yet, as the impacts of climate change become more painfully obvious, jurisdictions from small towns to the world’s largest countries are working towards solutions. Since the Regional Greenhouse Gas Initiative (RGGI) began in the Northeast, the Governors of the participating states have led by embracing, implementing, and improving a first-in-the-nation carbon reduction program. It is now up to a new group of Governors to determine whether RGGI remains a model for ambitious action on climate.

What does RGGI leadership mean?

Looking out for our climate, our health, our economy

Thanks to RGGI’s track record, the participating states can lead on climate without setting back their economies. As detailed in our recent report, since RGGI began CO2 emissions have fallen sharply (faster than the rest of the country), electricity prices have decreased (while the rest of the country has seen an increase), and the economy has grown (outpacing the rest of the country).

Change in Economic Growth, Emissions and Electricity Prices, 2008 to 2015

By setting ambitious cap levels for the future, the RGGI states can continue to achieve the best outcomes for our climate, our health, and our economy. Specifically, the RGGI states should establish post-2020 cap levels designed to meet existing climate targets, which cluster around 40% reductions by 2030. Analysis from Synapse Energy Economics has shown that implementing a RGGI cap with a 5% annual decline from 2020 through 2030 would be the lowest-cost pathway to achieving climate requirements. According to that study, such a cap would also yield over $25 billion in total savings for the region while creating 58,000 new jobs each year in the participating states.

A forward-going 5% annual reduction would be more gradual than what the RGGI states have achieved to date, but it would still put us on a path to achieving our science-based goals. And as we cope with the fact that global CO2 concentrations have now eclipsed 400 parts per million, it’s become more important than ever that our leaders address scientific imperatives on climate change with comparably ambitious policy.

The forefront of climate policy

When a bi-partisan group of Governors of the RGGI states first came together to place a limit on CO2 emissions, they staked their claim as national leaders on climate. In the absence of federal climate policy, they were the first states to act on reducing CO2 emissions from the power sector. When they decided to auction allowances rather than give them away for free—as was common practice under previous emissions trading programs—they directed billions of dollars to consumers instead of polluters. This decision is largely responsible for RGGI’s success as a program that reduces harmful emissions and serves as an engine of local and regional economic growth.

While the leadership role of the RGGI states to-date is indisputable, the bar for climate leadership has been raised. Since the RGGI program began, the region, the country, and the world have taken great strides to address carbon emissions. In recent months the U.S. and China, the planet’s largest emitters of CO2, have ratified the Paris Climate Agreement. In the last week, India and the European Union have followed suit, bringing the tally of signatories beyond the threshold of 55 countries and 55% of global GHG emissions necessary to make the agreement binding. Also this week, Canada—America’s largest trading partner—announced nationwide carbon pricing. Provinces can implement their own cap-and-trade programs (as Quebec, Ontario, and Manitoba have done), their own carbon tax (like British Columbia), or they can accept the federal carbon tax, beginning at $10/ton in 2018 and rising to $50/ton by 2022.

The RGGI states are no longer going it alone on climate, but they can still be leaders. Committing to a strong future for the program will provide a valuable guidepost as the rest of the country prepares to comply with the Clean Power Plan, and as the rest of the world considers how to reduce emissions without sacrificing growth. Momentum is building, support is growing, and the market is transforming – will the RGGI states continue to lead the way?

Reforming Electricity Pricing Can Promote Electric Vehicles and Help Optimize the Electric Grid

Electric vehicles (EVs) provide multiple environmental and consumer benefits. Because they emit about 60% less greenhouse gas (GHG) than conventional vehicles, EVs are an important element in reaching state GHG reduction requirements. Plus, EVs have lower operating costs than conventional vehicles—even with today’s low gasoline prices; for example, in Connecticut an EV only costs about five cents per mile to operate compared to eight cents for a conventional vehicle. That’s a savings of over 80 cents per gallon-equivalent. Given that the largest source of GHGs in the Northeast is the transportation sector, states should be pushing for accelerated adoption of these vehicles.

Recognizing this opportunity, many states in the Northeast have already committed to increasing the number of zero emission vehicles, primarily EVs, on the road by signing on to the California Clean Car Standards and the Multi-State Zero Emission Vehicle Memorandum of Understanding (ZEV MOU). These agreements have set an ambitious goal of increasing the vehicle fleet in those states to about 13% EVs by 2025.

Though this goal alone is commendable, concerns must be addressed about the amount of electricity that will be needed to charge these additional EVs. If EVs are plugged in during periods of high demand, they can strain the electricity system, triggering costs associated with increased distribution or transmission investment, greater capacity needs, and higher marginal energy prices. If EVs are charged at off-peak times, however, the impact on the electricity system is minimal and can even have benefits.

To encourage off-peak charging, several states have started to adopt electricity rate structures for EV owners that reflect the higher cost of providing electricity during peak periods and the lower cost during off-peak periods. These “time-of-day” rates typically divide the day into two or three different periods, during which electricity costs are different. “On-peak” periods encompass most of the afternoon and evening and have the highest rates; “off peak” periods comprise the rest of the day and weekends and feature lower rates; and sometimes “super off-peak” periods are offered with extra low rates from midnight to early morning when there is minimal demand on the system.

Because lower charging costs translate to lower costs per mile traveled, EV owners have a monetary incentive to charge during off-peak hours. This per-mile savings also makes owning an EV more attractive and can provide the extra push some consumers need to purchase an EV.

Pilot programs adopted by Maryland and New York have demonstrated that time-of-day rate structures are effective at shifting customer behavior. The chart below shows the electricity use of EV owners in Maryland before and after they adopted the time-of-day rate structure or “tariff.”1 Pre-EV tariff, the customers’ peak energy use was at about 6:00 pm (red line), indicating EV charging likely occurred when commuters returned from work and plugged in their vehicles. This peak also corresponds with peak system demand. Following the EV-tariff adoption, the peak use for the pilot participants shifted to 10 pm (green line), indicating that customers had altered their behavior to take advantage of the lower rates.

A poll of the Maryland customers who adopted the EV tariff found that over 90% of participants were either “extremely satisfied” or “satisfied” with their new electricity plan, and the majority of customers saved money on their house electricity bill. With the positive result of this pilot and others, Maryland and other states, including California and New York, are now offering full-scale (non-pilot) time-of-day rates for EV owners.

Given their demonstrated success, both satisfying customers and shifting behavior, time-of-day rates should be considered by states as one of the key mechanisms for meeting ZEV commitments and GHG emissions reduction targets. This single reform offers multiple, important benefits: it incentivizes owning an EV, it reduces the contribution of EVs to peak load, and it helps capture the significant environmental benefits of EVs—not just GHG emissions reductions, but also local air pollution reductions that help improve public health.

The Public Utilities Regulatory Authority (PURA) of Connecticut is currently considering whether to move forward with time-of-day rates for EV customers.2 As one of the 8 states committed to the ZEV MOU, Connecticut, through PURA, should make the smart choice to implement this proven reform as soon as possible. As Connecticut is likely not on track to meet its mandatory 2020 GHG emissions cap,3 and because transportation emissions comprise 40% of the state’s total GHG emissions, Connecticut will absolutely need the help of time-of-day rates. Acadia Center is participating in PURA’s current docket to ensure that it considers the environmental and consumer benefits of both EV adoption and time-of-day rates.

1 BGE Electric Vehicle Rate Pilot Program Report, February 2016

2 PURA Docket No. 16-07-21. Acadia Center has been granted status as an intervenor. Final decision scheduled for February 2017.

3 Acadia Center, “Updated Greenhouse Gas Emissions Inventory for Connecticut,” June 13, 2016. Emissions overall have increased 7.5% from 2012 to 2015 and we anticipate them increasing even more in 2016.